How to Finance as a Contractor

In construction, work doesn’t get paid up front. You mobilize, buy materials, put your crew on site—and often wait 30, 60, or even 90 days to get paid. If you’re growing, those timelines stretch your cash even thinner. Suddenly, you’re juggling payroll, covering vendors, and figuring out how to float the next job while waiting on checks from the last one.

In this post, we’ll show you how to finance as a contractor—not by relying on expensive short-term debt, but by building a smart plan that gives you control over your cash, protects your margins, and supports growth. For contractors and specialty trades generating $3M–$30M in annual revenue, this isn't just about staying afloat—it's about unlocking the capacity to scale without chaos.

Key Takeaways

-

Construction businesses face unique cash flow timing challenges

-

Financing should support growth—not patch gaps

-

Strategic forecasting and internal systems are just as important as outside capital

-

The right mix of financing tools gives you flexibility without unnecessary risk

The Real Challenge: Front-Loaded Work, Delayed Pay

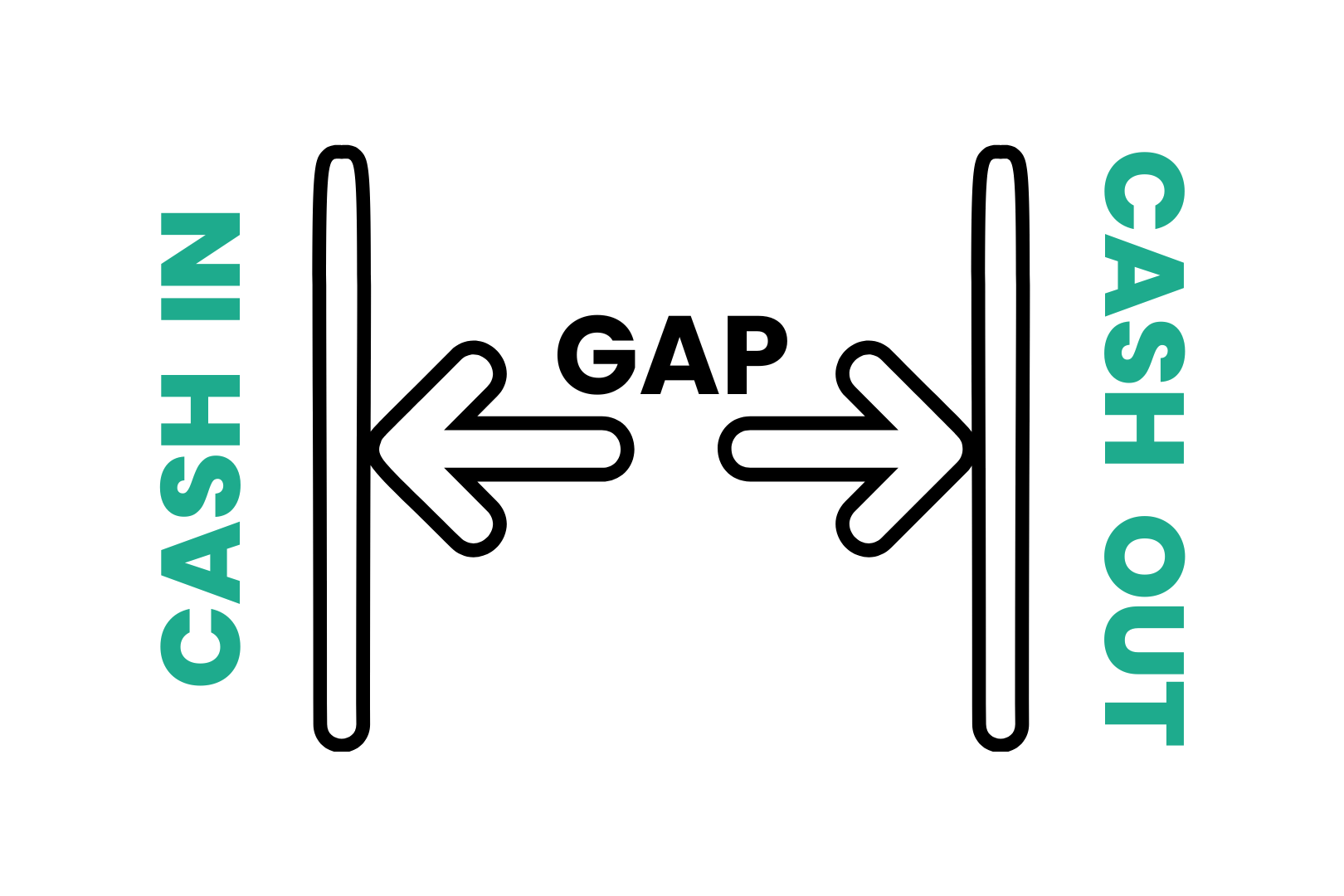

Contractors don’t get paid for showing up. You get paid for progress—once it’s billed and approved. But between retainage, slow-moving GCs, and project delays, that money often lands long after the work starts.

This creates a gap between cash out and cash in. The larger the job—or the more jobs you take on at once—the more capital you need to cover labor, materials, equipment, and overhead up front. Without a plan, that gap becomes a bottleneck. It’s not uncommon for growing contractors to win more work than they can afford to deliver—simply because they haven’t built the financial foundation to support it.

And it’s not just about getting paid—it’s about timing. You might have great revenue, but if the collections don’t align with the outflows, you’ll still feel the squeeze. Financing, when used strategically, helps you bridge those gaps and move forward with confidence.

Understand Your Financing Options

Contractors have more tools than most realize—but each comes with trade-offs. The goal isn’t to rely on financing forever. It’s to use capital to gain leverage—to win better jobs, smooth out cash flow, and expand at the right pace.

Here are a few of the most practical financing tools available to construction businesses:

-

Lines of Credit: Flexible, short-term capital to cover payroll or materials while waiting on receivables. Works best when managed with discipline and paired with a forecast.

-

Equipment Loans or Leases: Free up working capital by spreading the cost of heavy machinery or vehicles over time. This keeps your cash available for labor and job-related expenses.

-

Mobilization Funding: Short-term capital tied to the upfront phase of a project—perfect for covering crew mobilization and initial costs before the first draw.

-

Material Trade Credit: Often overlooked, negotiated supplier terms can reduce upfront outlay without increasing debt.

-

SBA or Construction-Specific Loans: For larger growth initiatives or working capital needs, longer-term financing with favorable interest rates may apply.

Each of these tools works best when paired with good planning—not desperation. Financing should be predictable, not reactive.

Forecast First, Then Finance

If you want to use financing the right way, you have to plan ahead. That starts with visibility into your cash flow—not just in general, but job-by-job. You need to know when money is going out, when it’s coming in, and how each project affects your overall position.

Start by building a 13-week rolling cash flow forecast. This shows your expected inflows and outflows week by week, including payroll cycles, billing schedules, equipment costs, and loan payments. When done right, it gives you a clear picture of when you’ll hit a cash gap—and how big it will be.

This is how smart contractors avoid surprises. You don’t need a crystal ball—just a system that connects your jobs, your overhead, and your financial obligations in one view. From there, you can decide exactly how much capital to access, when, and through which vehicle—without overextending yourself or pulling from the wrong source.

Strengthen Internal Systems Before Scaling

Financing can solve short-term problems, but if your internal systems are weak, it will only mask deeper issues. Many construction business owners think they need more cash—when what they actually need is better financial structure.

Before you increase credit lines or take out a loan, make sure you’ve tightened the foundation. That includes consistent job costing, clean invoicing, timely change order tracking, and active collections follow-up. If your project managers aren’t aligned with your financial team, or your WIP reports are out of date, you’ll end up borrowing to fix what better systems could prevent.

The best contractors run lean and structured. They know how much every job costs, how long it takes to get paid, and exactly what’s in backlog. With that level of clarity, financing becomes a growth tool—not a lifeline.

Final Word: Fund the Work, Not the Chaos

Financing as a contractor doesn’t have to mean stress. When you build the right systems and use the right tools, financing gives you power. It lets you take on bigger jobs, retain top talent, and grow into a business that leads—not just survives.

At Coltivar, we help contractors and specialty trades build financial structures that allow them to use capital strategically—not emotionally. Because when your money flows as smoothly as your fieldwork, your business becomes unstoppable.

Want to finance your growth without draining your cash or increasing your risk?

Book a Strategy Review and we’ll help you build a system that works for your next stage.