How to Make Your Company More Valuable

Think revenue is what drives your company’s value? Think again. In this video, Steve shares two overlooked levers that can dramatically increase what your business is worth—based on real insights from his experience acquiring companies as a CFO.

You’ll learn what most business owners miss when it comes to valuation, and how to shift your focus to the factors that truly move the needle. If you want to build a more valuable, more sellable company, this is the place to start.

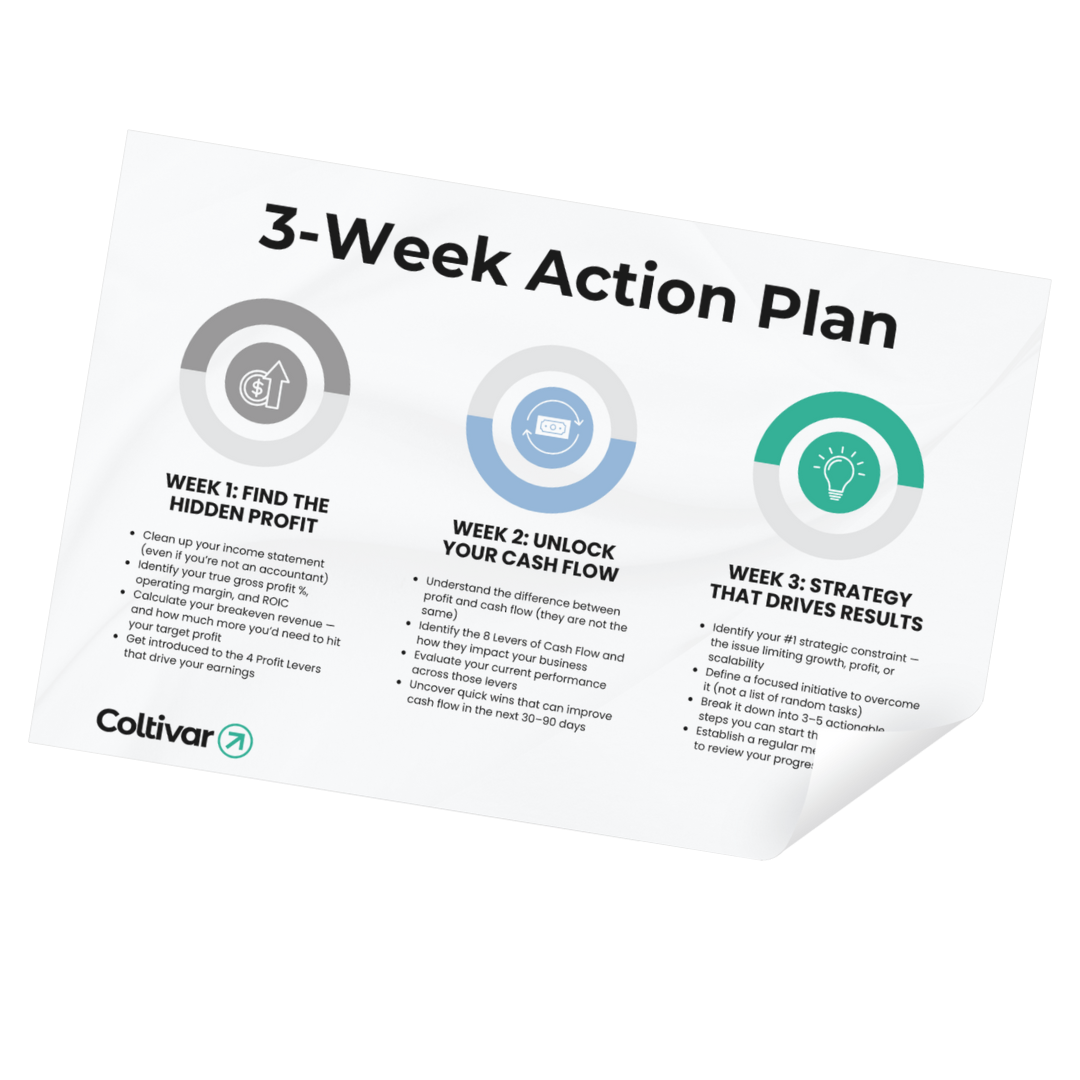

The 3-Week Plan to Grow Without Chaos

Learn how to take back control of your time, streamline your operations, and build a business that scales — without burning out.

Get my personalized planTRANSCRIPT:

Spoiler alert, revenue doesn't drive the value of your business. There are plenty of $10 million companies out there that can't even sell for $1 million, while others sell for 8x their profit or even more. You might be growing, but are you actually building value? In this video, I'm going to leave you with the two ways to increase your company's value. So by the end of this, you're going to know exactly where to focus. Let's go ahead and jump in.

When I was a CFO, I did a lot of M&A. I was buying a ton of companies, and I'm going to tell you the two ways to increase value, especially from this perspective, which is really important. Number one is through EBITDA improvement. EBITDA is just a fancy way of saying profit. It stands for earnings before interest, taxes, depreciation, and amortization.

In fact, when it comes to valuation, this is the multiples-based approach. Really, it just involves taking EBITDA or some other financial driver. Maybe it's revenue for your business. Maybe it's cash flow. But for most companies, EBITDA is the most standard, so we'll stick with this. If you take EBITDA and you multiply it by a factor, a multiple, it'll tell you what the value is of a company.

So in other words, let me just map this out. Value, using the multiples approach, is determined by taking EBITDA—can’t even spell here—EBITDA times a multiple. This is just a shorthand way to determine valuation. Now, there's a more complicated way. You can take the income approach, build a discounted cash flow model. I'm not going to get all nerdy on you right now because we don't need to focus on that.

So instead, we can focus on this. In order to increase EBITDA, there are four levers to pull. That's it. Just four. Alright, so you could totally remember this.

Number one is pricing. So you can increase the pricing for your products and services. We'll get into that here in a second. Next, we have volume. This just involves selling more units.

We also have cost of goods sold. These are all the costs associated with delivering the product or service—in other words, fulfilling the product or service that you're selling. So there's cost of goods sold, and then we have OPEX, which is just shorthand for operating expenses.

So you can increase pricing, you can increase volume, you can decrease COGS, and you can decrease overhead. Those are the four levers to pull. Alright, do you know that out of these four, there is one that is far more superior than the other ones? And this is for most businesses. There may be some nuances or exceptions, but generally speaking, guess which one it is?

If you said pricing—you’re absolutely correct. On average, I'm just going to put it's like 12%. Alright, now cost of goods sold is actually number two. So if you can make your cost of goods sold more efficient, it's about 7%. Volume is about 4%, and OPEX can be about 3%.

Now this depends on companies, industries, etc. If you want to know exactly what your levers are and the impact you'll have on profit—in other words, for every 1% change in each of these levers, this is what you're going to get—that's what I was telling you right here, the 12%, 4%, 7%, 3%. It just represents a 1% change on any of these levers.

If you want to know what the exact number is in your business, go to coltivar.com. Under Resources, we have calculators, and you could pull up this calculator. You could plug in two numbers in your business, and it'll spit out exactly what the numbers are for your company, which is super valuable because think about it like this.

Let's say you're communicating to your sales team, and you're like, look, for every 1% discount we give our customers, it's going to have a 12.3% impact on our bottom line. I just made that up. But, right, that's so much more powerful because it's specific. Instead of just saying, hey, don't do discounts because we lose money. Like, get specific, understand what your levers are, and then you'll be able to influence EBITDA, which is this first part of the equation.

Now, I'm starting to help you out. Can't you see the value in this? Because you may be feeling like you've worked so long, right? You've worked so long, so hard on your business. You've poured a ton of energy, blood, sweat, and tears, capital into your company, and you don't even know what it's worth. Well, I just uncovered that for you right here.

And the first part—we're going to get into the second lever here in just a minute. But if this is making sense to you, can I get a yes in the comments box below? Okay. Just drop yes. So I know you're following along.

Okay. All right. Let's talk about number two. And then at the end, I'm going to share with you how I use these levers as a CFO and tie everything together to maximize the value of the companies that we were buying. It's really cool and really powerful. All right. But let's get into number two here.

And this involves multiple expansion. Pretty easy, right? See, you totally got this. I gave you the formula. And when you understand the formula and you could break it down mathematically like this, and you'll know, okay, this is a driver and this is a driver. And that's ultimately what I'm showing you here.

Now, here's the deal. When it comes to valuation, the multiple is just shorthand for a lot of other things. It's trying to estimate things such as risk, growth, retention of revenue, etc. There are a lot of things. And when you break this down even further—like risk—you have key person risk, key man risk. Okay. That could be a man or a woman.

You have key customer risk. You may have systems risk. You may have data risk. And there are some other risks in here. But this is what the multiple does. So essentially when somebody comes to you and they're like, okay, I'll buy your business. Here's your EBITDA. And the growth of the business looks really promising, but the risk—like you're the key person in the business. You don't have systems documented. Therefore, I know if you leave, I'm going to lose money. I'm going to lose profit. So therefore they discount this multiple.

Same thing with retention. If you don't have a sticky revenue base, meaning that your revenue is all over the place, or you just have to go out there, get work, do work, get work, do work—like in construction—this is going to impact your multiple. So you can do things from a strategy perspective to fix this. In other words, you can put in place systems. You can document SOPs. You can position yourself in a market where you have better retention. You can offer new products and services that are more sticky, etc. You can position yourself in a market or in a segment where growth is looking good. So you can do all these things and that will give you multiple expansion.

So here's an example. When I was a CFO, we would go into these businesses and we would buy them for 2x EBITDA for a variety of reasons. Now, some of them were more successful and we would pay sometimes 3x EBITDA, but typically these were somewhat smaller businesses. Now you may be wondering what's the average EBITDA multiple. It ranges, it varies, but if you want me to spit out a number, I would say most businesses are like 2.5 to 3x EBITDA. It depends.

So we go out there and we look at the company. We look at EBITDA. We would buy them for 2x to 3x. So say we bought a $10 million business and we paid 2x. Ultimately, we spent $20 million on the acquisition. Okay. So let's just say we did this 2x, 10 million, 2x. I'm simplifying here. That's not what we did. They had different prices, but just keeping it really simple in this example. So we paid 20 million, 20 million, 20 million. And this combined together is we paid $60 million.

But we did this with a combination of debt and equity. So we have a little bit of leverage going on here too. But then by combining these companies right here into one enterprise, and then putting in place a strategy to transform them from a subscription-based business—that's what they were in—to a data-based business, a data-driven business, just by doing that switch and changing the market focus and position and tweaking the product and service, we were able to take this 2x ratio to 6x.

So now even without improving EBITDA, we have 30 million in EBITDA times six, that's $180 million. We just 3x’d our investment just by putting these companies together, changing their product mix, and then changing the market focus and position. Pretty powerful. I mean, it's not like it's, oh, you just do that and it's easy. It took a lot of work and it took a lot of members on the team, but here we go.

Now the other lever we could pull, like I said, is EBITDA. So we'd go in there and improve these companies by focusing on these four drivers. And we were able to increase it, and let's just say to 50 million right here in EBITDA. So now you add the 6x and you end up with 300 million right here in valuation.

And that's the power that I want to drive home today is that you can improve the financial and operational performance of your company, which is going to drive higher EBITDA, but you can also apply strategy and you can fix these things down here and you have to do it in advance. And if you do that, it's a major difference in your end game.

So think about it. If you're planning on selling your business and you want to be out in say one year, three years, five years, you have to start planning right now today. Even one year is ambitious. Sometimes it'll take three years just to turn around a company, just to put in place the processes and systems, just to get it ready to sell.

And if you rush this, or if you don't invest in fixing this or putting in place a strategy or a system to make this all happen, guess what? You could be selling your business over here for $20 million when the real value is like 60, which is insane. You don't want to get to the point where you're burnt out, where you're exhausted, where you don't want to do it anymore. You sell the business and you walk away from tens of millions of dollars. I've seen it happen all the time because there's not advanced planning, right?

If you want to talk about this more in your business, you can always reach out to us at coltivar.com. And we also have a lot of tools and resources that are free. So you can just go to our platform and check out what we've prepared for you. There's a lot of value there, but that's what I have for today. Until next time, take care of yourself. Cheers.