You’re Profitable—So Where’s the Cash?

Your income statement says you made a profit—but your bank account tells a different story. In this video, Steve explains why so many small business owners feel cash-strapped even when they’re showing strong profits on paper.

You’ll learn where cash flow really hides on your financials, how to spot the traps that quietly drain your liquidity, and what to do to keep more money in your business. If you've ever asked, “Where did all the money go?”—this video will give you answers.

Subscribe for more practical strategy and finance tips to help you run a stronger, more resilient business.

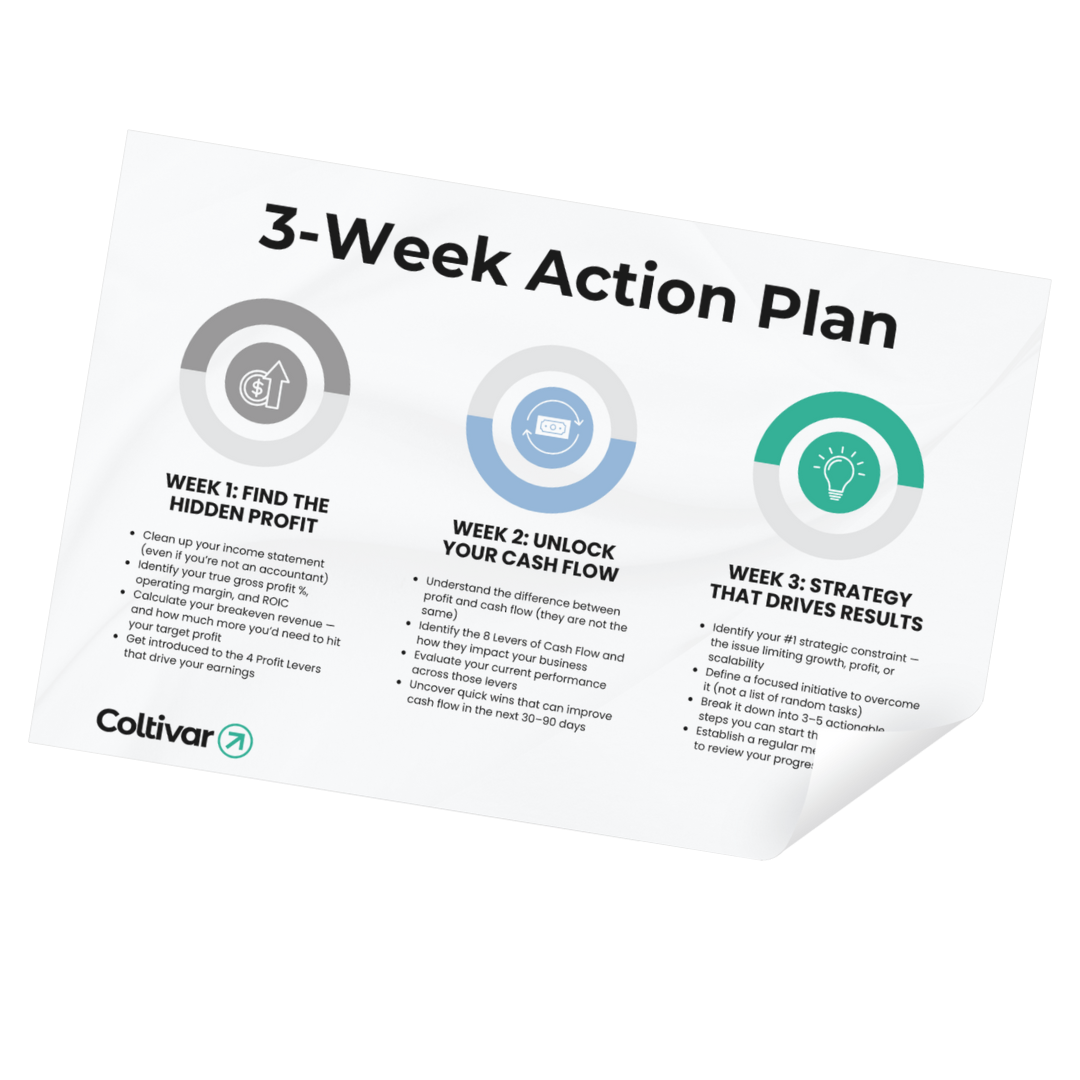

The 3-Week Plan to Grow Without Chaos

Learn how to take back control of your time, streamline your operations, and build a business that scales — without burning out.

Get my personalized planTRANSCRIPT:

Your income statement says you made $500,000 in profit, but your bank account is nearly empty. If this has happened to you, don't worry, you're not alone. This is one of the most frustrating and confusing problems in business. And here's the good news, by the end of this episode, you're going to know exactly where to look to identify problems or future problems, and more importantly, how to fix it. So let's go ahead and jump in.

So the first thing you need to do is look on your income statement. So here's the income statement, and at the top of your income statement, you have a revenue. Revenue represents the income that's generated from selling your products and services. So you have revenue, then you have cost of goods sold, COGS for short. You take revenue minus cost of goods sold, you end up with gross profit. I'm abbreviating here. Gross profit then leads to OPX, which is your income statement. Your operating expenses, take gross profit minus OPX, and you arrive at operating profit. There are some other things like other income and expense that you account for, and then you arrive at income before taxes. Now, depending on the system that you use for your accounting, it may say net income, but nonetheless, it's the bottom line of your business.

So you look here and you have $500,000 in profit, and you're like, we're good, right? We're solid. But then you look at your bank account and you're like, we don't have the cash. We can't even cover payroll. I'm going to have to pull in the line of credit. I'm going to have to take money out of my personal savings account and put it in the business just to make things work, right? Have you felt like this? If so, type yes, in the comments box, because I'm sure you felt like this. I felt like this before. I've been in this exact pickle before. And I didn't know how to fix it when I was running my first company, because I was young. I was in my late teens, early twenties, when I reached over a million dollars in revenue. Here I was running this multi-million dollar business, in fact, and I had no clue how to read an income statement or balance sheet. So that's why I say you're not alone.

So this is just profit. But the problem is, is that profit is not cashflow. And cash is what makes your business work. This is what keeps you liquid. So where are the other components that get you down to cashflow? Let me walk you through that. Now you may be wondering, like, I have no idea where my money is going in my business. And don't worry, just hold on. By the end of this video, like I said, you're going to know exactly where to look in your company.

On the balance sheet, okay, you have assets, liabilities, and equity. In fact, the accounting formula is assets equal liabilities plus equity. This is how a balance sheet balances. Now under assets, you have current assets, and under liabilities, you have current liabilities. Now current assets and current liabilities represent all the items that are due and payable or collectible within 12 months. So when you see current on your balance sheet, just think within 12 months, you're supposed to collect on this or pay on this. So if you take current assets minus current liabilities, and I'm just going to keep things really simple here. But if you just take current assets, current liabilities, there are some nuances, but this will get you close enough. This will tell you what you're working capital is. So that's a big thing right here. We have working capital.

Now you may be wondering, okay, what the heck is in working capital? Well, there are three main things. There are some other things, but let me just give you the big categories. First, you have accounts receivable. This represents the amount of money that your customers owe you. You have inventory, typically, and you have accounts payable, which represents the amount of money you owe your vendors. So if you go buy supplies, you put it on account and you say, Hey, I'll pay you in 30 days. This is showing up in accounts payable.

Notice that this money, this cash, which is on the balance sheet does not show up on the income statement. It shows up here. And let's just say your business has $400,000 in working capital. That means you are going to be at $100,000 less in cash. Assuming that this profit equals cash, which it doesn't, I'm simplifying there's depreciation, there's amortization, there's taxes, there's all that stuff, but let's just keep things simple in this video. If you want to get more detailed, I'll do another video later on that. Okay.

So you have profit, you have to account for working capital. I just showed you where that is on your balance sheet. Now there's one other financial statement. I'll just draw over here, which is the statement of cash flows. And the statement of cash flows has three sections. You have cash from operating activities, cash from investing activities, and cash from financing activities. If you look under investing activities, you should see a line called capital expenditures or CapEx for short. This represents all the monies that's paid to buy things like trucks. Here's a truck, right? To pay for a building. Here's a beautiful building with a tree, right? Terrible building, but it's all your assets. You buy a truck, you buy tractors, etc. All those investments represent CapEx.

Now, a side note on the balance sheet, you have non-current assets, which includes your property, plant and equipment. And if you look at this period over period, and you do some adjustments for any equipment that you sell and depreciation, etc., then you could find CapEx as well. But I would say the easiest thing is just to go to your statement of cash flows and you'll see this number here. So CapEx once again, doesn't show up on the income statement. So we have CapEx. The only thing that's showing up on the income statement is when you depreciate your CapEx.

So in other words, you go buy this truck for $50,000. You can't just record $50,000 as an expense on your income statement, because remember, you have to match your income and your expenses in the same period in which they occur, right? In which the economic value is realized. And it's not like this truck is going to last one year. Well, hopefully not. Hopefully you don't drive it like it's dirty, you know, drive it into the ground. Instead, this is probably going to last for five years. And let's just say it has a zero value at the end of five years. That means you're going to depreciate 10,000 a year. So this depreciation shows up on the income statement, but what about the other 40,000?

And this is where businesses get into a serious trap because they don't understand how much money they're actually reinvesting in their capital expenditures. And let's just say for this business, it's $200,000. So they bought a bunch of tractors and trucks, etc. And guess what? If you add all these up, like I said, I'm simplifying. There are a lot of nuances. Trust me. I could get way more technical and nerdy, but I'm not because you don't really need to understand all that at this point, but this means that you would have a hundred thousand in negative cash.

So the question is, where are the issues? Like where are the hidden, you know, dead bodies? They're on the statement of cash flows and they're on the balance sheet with working capital. And if you don't watch these two things, working capital and CapEx specifically, you can show profit on your income statement, but you don't have the cash.

There's one other thing. This is a little bonus for you. Under equity. There's this thing called distribution distributions, plural or dividends. It's basically money that you take out of the company to pay yourself as an owner or stakeholder in the company. Guess what? These distributions and dividends are cash out the door. They're not on the income statement. So you also have to account for this. So if you're a business owner and let's just say you're taking a meager salary, but you're taking a lot of distributions, that's totally fine, but it's not tracked once again in profit it's over here on the balance sheet. So this can even exacerbate the problem and make it even worse.

So as you can see for this company, we just saw a $500,000 in profit go to negative $100,000 in cash. Like I said, I'm simplifying add on distributions and dividends. And you can see why 70% of companies that go bankrupt are actually profitable when they close their doors.

So how do you fix this? If your working capital is high, make sure you're managing AR. And if you don't have a KPI already in your business, key performance indicator, make sure you're tracking AR days. And let's say your terms are 30 days with your customers. Well, your AR days should be around 30 days or less. That's when you're managing your AR really well. But some companies like what I'm working with recently, their AR days are at 60, even though their terms are at 30. And guess what? That means that the business is bankrolling that. Okay. So this could be a problem.

Inventory, you may be sitting on a lot of inventory. I can't tell you how many retail shops I go into and they have so much inventory, all these shirts and all this junk merchandise that's not moving. So just in time inventory, better inventory management is key because all that stuff on the shelf in the back of your office is cash. It's like cash sitting on the shelf.

And then AP, let's just say you have 30 day terms with your vendors. I know some of you are like, I don't like to owe people money and I like to pay them fast. Well, let's just say your AR days are 30 because you manage your AR well, but your AP days are 15 because you get a bill from your vendor and you just pay it, right? Even though your terms are 30 days. Well, guess what? This Delta between 30 and 15, you're bankrolling that as well. So that's how you can improve working capital.

With CapEx. I would just say, this comes back to strategy and it's all about having a strategy where you can build a business that's asset light. If your CapEx is greater than 25% of your revenue, this could be a major problem, right? Because it means that every dollar that comes in the door, you're spending 25 cents on equipment and trucks and your building, etc., just to produce that revenue. And that could be unsustainable. So put a place, a strategy that allows you to build an asset light business. Make sure you don't over-invest in this.

When I was in my early twenties, I would go out there and buy the most expensive work vehicles and I'd just overspend. I'd over-invest compared to what we actually needed. Then I got smarter and I was like, all right, we're going to start buying trucks with 240 AC. That's the joke. 240 means two windows down, 40 miles an hour. Okay. 240 AC. But all kidding aside, we started to buy trucks that were more economical. We saved a lot of money on the CapEx and that really helped our cashflow.

So those are just a few tidbits for you. Also, if you're a business owner and you're taking distributions, having consistency in a schedule will help you with lumpy cashflow. So you know exactly when you're taking these distributions and you can plan it out.

All right. What do you think? Is this helpful? Can I get a yes in the comments box? So I know that this is valuable stuff to you. And plus you can leave comments and let me know, what other types of topics are you most interested in?

All right. That's what I have for you. If you want to learn more about this in your business, if you want to create a dashboard for your company, so you can track this stuff in real time, you can always connect with us at coltivar.com and my team can show you exactly how we can make this work for you. And until next time, thanks for tuning in. Take care of yourself. Cheers.