What Is Free Cash Flow?

Most businesses don’t fail from lack of profit—they fail from poor cash flow. In this video, Steve breaks down what free cash flow really is, why it matters more than profit, and how to avoid the most common cash flow mistakes.

You’ll learn how to go from revenue to net operating profit to true free cash flow—and how to use that insight to run a healthier, more valuable business.

If cash flow has ever felt confusing, this video will give you the clarity you’ve been missing.

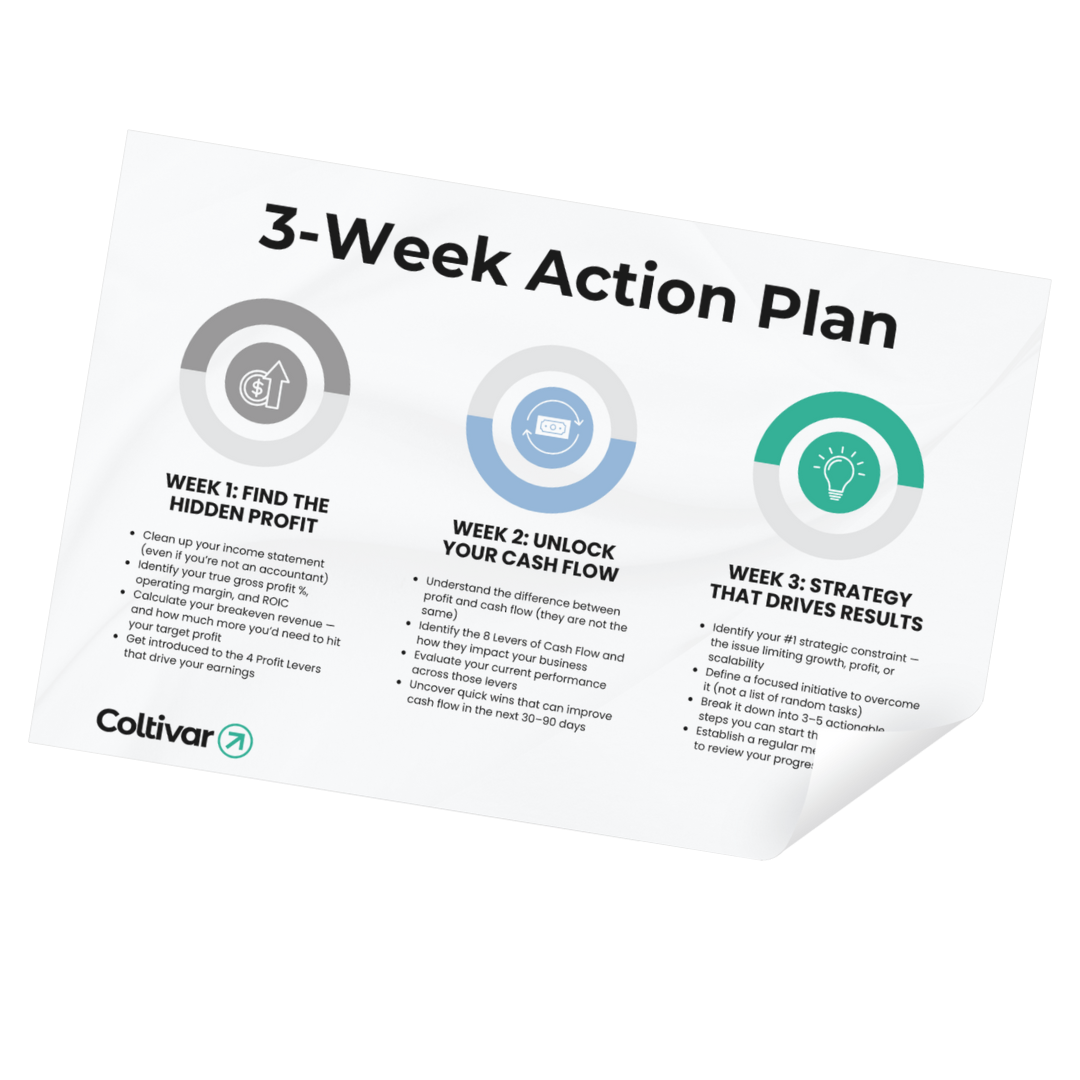

The 3-Week Plan to Grow Without Chaos

Learn how to take back control of your time, streamline your operations, and build a business that scales — without burning out.

Get my personalized planTRANSCRIPT:

If cashflow is confusing for you in business, causing you to avoid financial decisions, or you're not even looking at the financial statements, I got you. You're in the right place. My name is Steve Coughran.

I'm the founder of Coltivar. I've spent my entire career turning around and growing businesses. And in the process, I've generated over a billion dollars in value.

And on this channel, I help business owners and leaders to understand cashflow so they can get more of it and increase the value of their companies. All right. So let's go ahead and break down cashflow from the very top.

When we look at the income statement, it begins with revenue. Revenue represents the sales of a company. It's the top line. It's all the income a business generates from selling its products and services.

Now, revenue is not profit. It's definitely not cashflow. So let's go ahead and keep breaking it down so we can get down to cashflow and you can understand how this all works.

The next line item is COGS. COGS is just short for cost of goods sold. This represents all the costs associated with fulfilling a product or service. It may include items such as direct materials, direct labor, contractors, and all other costs associated with getting the product or service into the hands of customers.

All right. So if we take revenue minus cost of goods sold, we arrive at gross profit. We're not talking about yucky gross. We're just talking about the profit before we account for overhead expenses.

The cool thing about gross profit is it will tell you whether or not your business is successful at selling the right amount of volume, at pricing its products and services correctly, and fulfilling the work in a cost-efficient manner. So if you don't have healthy gross profit, be sure to check your volume, your pricing, and your cost efficiency.

All right. Below operating profit, we have OPEX, which is just short for operating expenses if you want to sound cool or maybe not so cool. Nonetheless, it's synonymous with overhead, SG&A, fixed costs. All of these terms are often used to explain operating expenses.

But at the end of the day, OPEX represents all the costs associated with running the business and can be broken down into three main categories. Number one, selling and marketing expenses. Number two, general and administrative expenses. And number three, research and development.

All right. If we take gross profit and we subtract out OPEX, we arrive at EBITDA. EBIT what? EBITDA is just a nerdy way of saying profit. It stands for earnings before interest, taxes, depreciation, and amortization.

The reason why EBITDA is so commonly used in business is because it's a great way to measure profitability on a comparative basis. What I mean by that is it ignores the capital structure of a business. That's why you don't include interest.

It also ignores the tax position of the company because every business has tax credits and all of these other things going on with it from a tax perspective. So it just eliminates that. And then depreciation and amortization, it doesn't account for those types of decisions, CapEx decisions, which I'll get into here in a minute.

So it's just a way to normalize profit. So you can compare it, like I said, from company to company, right? I could do a whole nother lesson on EBITDA, which maybe I'll do in the future. Just let me know in the comments down below, if you like this format, if you want me to talk more about any of these topics that I touch on, just drop that down below, and then I'll know what to do future videos on.

All right. So we have EBITDA here, and ultimately I'm trying to get you down to free cashflow. So we have to take out depreciation and amortization. I'm going to explain that here in a second, but after we do that, we are going to arrive at EBIT. So we just drop the DA.

Now we have earnings before interest and taxes. Okay. So here's the thing with depreciation and amortization. I don't know why it was so confusing, at least for me back in school. Maybe it's just because I'm a slow learner, but depreciation is when you are accounting for the economic benefits or the depletion of an asset, of a tangible asset, and amortization is when you do the same thing, but for intangible assets.

So depreciation is tangible. Amortization is intangible. Let me give you an example here.

Let's say you go buy a truck. Here's a truck, and there's a cat driving the truck. I don't know why there's a cat, but a cat's driving the truck, and this truck, let's just say, is 50K, and maybe it has some spinners on it, has some really sweet rims, whatever.

Okay. So you have this truck. It's $50,000. Well, according to GAAP, Generally Accepted Accounting Principles and IFRS, International Financial Reporting Standards, or the IRS, you can't just take this $50,000 and expense it. You can't just record it in OPEX or Cost of Goods Sold.

Here's why. Because of the matching principle. The matching principle says you should record the economic cost or the benefit of something in the period in which it's incurred or realized.

So in other words, all the fancy talk put aside, to put it simply, when you have revenue, you want to record revenue. Then you want to record all the expenses associated with that revenue in the same time frame. Otherwise, your financials are going to be a total mess.

So with this truck, this thing's going to last, let's say, five years. If you record this entire $50,000 in the first month of the year, well, guess what? That's going to totally skew the financials, and it goes against the matching principle.

Therefore, what you have to do is you have to take $50,000. We'll say, okay, it's going to last five years. Take the useful life, five years. That means you can depreciate it 10K per year for five years. That just assumes that after year five, it's going to have a zero value, zero salvage value. So we're just keeping things simple.

Now, the reason why I said depreciation is because it's tangible asset. It's something you could touch, feel, massage, rub, wax, whatever you do with your fixed assets, but that's what it is.

Okay. So that's depreciation and amortization. And for tax purposes, you can write off the economic usage, the depletion, this $10,000 per year for tax purposes.

Okay. So that's what we're doing here is we're accounting for depreciation and amortization. Back to EBIT, earnings before interest in taxes. My license plate actually used to be EBIT because in Colorado, somebody took EBITDA. I think a lot of people thought it was some type of cryptocurrency because they're like, what is EBIT? So anyways, I could have messed with them a lot more than I did.

So we have EBIT. Then fortunately or unfortunately, we have to pay for taxes. And we take out taxes from this and we end up with NOPAT, Net Operating Profit After Tax. See all these cool little acronyms you can incorporate in your daily conversation or at your dinner table.

Okay. Maybe not. All right.

So we have NOPAT here. This represents the profit, the operating profit of the business after taxes. The reason why I differentiate operating versus not operating is because we have these other items over here. Other income and other expense.

That is not core to the normal operations of the business. We don't want to account for these things because it will skew how much cash flow the business is generating from normal operations. So for example, other income may include interest income. And unless you're a bank in the business of earning interest as revenue, you're going to exclude it.

The same thing is true with interest expense. You're going to exclude that. Let's say you have a gain on a sale of a piece of equipment or some type of asset. You don't want to record that gain down here. You want to record the gain here in other income, which is not operating, unless you're in the business of selling equipment.

So we want to include everything that's not core to the business over here. We're going to exclude it from this free cash flow calculation. It is going to show up on your financial statements. It is going to be a part of getting you down to net income, but it will not be a part of free cash flow.

Okay, carry on. This could be a whole other conversation too. So we have NOPAT, net operating profit after tax, how much profit we're spinning off from operations.

Then we want to get to cash flow. So guess what? We have to add back items that are non-cash. So depreciation and amortization.

Remember, we're just depleting this truck over this five-year period to be compliant with the IRS and GAAP and IFRS, right? And we want our books to match economic reality. So really, we're just doing an accounting exercise to record the depletion here for taxes and whatnot, and to capture the economics of the business.

But it's not really cash out. It's not like we're writing a check to Mr. or Mrs. depreciation and amortization every month. So there's no cash outflow because the cash outflow came through CAPX.

CAPX represents capital expenditures. So when we buy this truck, let's say we took 50K, right? 50K in cashola, right? Here's our little cashola, right? We spent 50,000 in cash to buy this truck. Well, that cash is a part of CAPX.

You can find this on the statement of cash flows under investing activities, FY. That's a little side note bonus for you.

All right. So we want to account for CAPX. And then we also have to account for changes in net working capital.

This is a big topic. I talk about this all the time, but I have to break it down into small chunks because otherwise it could be super overwhelming. So from a simplicity standpoint, check this out. It's just current assets minus current liabilities.

There are some other nuances here where you're going to account for excess cash, and you don't want to include interest bearing current liabilities, right? So those are some nuances there, but you're going to look at the change in current assets and current liabilities from one period to the next, right? So it's this change that's flowing down here in our calculation to get us to free cash flow.

All right. Net working capital, like some examples of current assets may include accounts receivable or inventory. Those are the big ones, not all of them, but those are the big ones. Current liabilities, the biggest one is typically going to be accounts payable.

So those are just some examples, but working capital is what the business needs in order to sustain operations. And therefore we're accounting for that change here.

We have now arrived at free cash flow. Now free cash flow is what makes a business work. Did you know that 70% of companies that go bankrupt, they're actually profitable when they close their doors, right? Don't believe me.

I'm going to show you here in just a minute, but really free cash flow is the lifeblood of the business because it does three things.

Number one, it allows the company to pay down debt, right? So it's all the cash after everything, after all the expenses, all the capex, working capital is accounted for. So you have some cash left over, you could pay down debt.

Number two, you can return that to equity providers. And number three, you can reinvest in the business. Those are the three uses of free cash flow.

And guess what? A business is valued based on its free cash flow. In fact, the intrinsic value of a business is defined as all the future cash flow that the business is going to generate over its remaining useful life in today's dollars.

All right. So that's why I love free cash flow. Let me just draw a little heart here because I love free cash flow so much.

All right. That's how you build a great business. A great business isn't one with a ton of revenue or a ton of profit, although they can be a great business is one that produces stable and healthy cash flow.

That's why I wrote this book, cash flow. This is my most recent book. I just published it. It talks about all the things that I've learned, all the experiences I've had as a CFO, CEO, investor, and advisor.

And check this out. I even have some like funny looking pictures in the book just to keep you entertained and to show you why I decided to stay in finance and not get into art. Okay. Enough of that.

But you can get a copy on Amazon in all different formats. I've made it as cheap as possible on Kindle, right? So Amazon will let me go lower than 99 cents. That's what it's priced at today as of this recording.

And also right now at Coltivar.com, you can get a free copy where I'll sign it. If you live in the continental US, all you got to do is cover shipping and handling. I'll cover the cost of the book.

But like I said, it's only as of today, later on, if you watch this video and I take away the offer, Hey, don't be mad at me. All right. That's just what it is, right? We're not done yet.

Are you ready for some bonus stuff? Check this out. Here's my experience as a CEO, CFO, investor, advisor to businesses, most managers. Okay. This is a manager right here.

Most managers live in this world right here between revenue, cost of goods sold and gross profit. They pay attention to sales. They're managing the costs, like all the labor, all the material, all the inputs that go into producing the product and they're measuring gross profit. All right. So we'll just put an M for manager.

Let's get some colors on here. Next we have between here and here we have business leaders. Here's business leader. Oh, she's got beautiful hair. She's kind of a scary girl. Okay.

Business leaders here. They are monitoring revenue all the way down to no path. This may be you. You may be looking at your income statement. You may be scared of the balance sheet. It's not that scary, but this is where I find most people living right here.

They'll build a forecast based on profit. They're looking at this in some form or function. Maybe your line items are a little bit different, but ultimately they're looking at profit.

Okay. But this is the key right here. Boom. I'm just going to draw right over this person. Sorry, person. I'm going to make this in red.

This is where I'll just call it value. I can't even spell that is terrible. Value creators. This is a term I use at coltivar, but value creators, they operate throughout the entire spectrum of free cashflow because they know, like I said before, 70% of companies that go bankrupt, they're profitable.

So they got profit right here, but guess what? They are not paying attention to this stuff down here, which is really important. This stuff can be found on the statement of cash flows or on the balance sheet by combining some things and doing some simple math.

But this is where you need to live as a business owner. All right. So I promised you I would break down free cashflow.

Hopefully this helps you to understand it a little bit better. Maybe you're not an expert yet, but I'm going to produce more and more videos just like this. You can really understand cashflow because like I said, the majority of businesses that fail, they fail because they don't have cashflow.

Leaders don't understand how cashflow works and therefore they can't forecast it. They can't improve it when it's going down the toilet and they struggle to increase firm value because there are all these distractions out there buying for everyone's attention. And if you don't focus on the most important things in the business, it's super easy to go straight, right?

That's what I have for you. I hope you enjoyed this video. Like I said before, please drop comments down below. So I know what other topics to cover and things that are top of mind for you so you can be more successful in business.

All right. Until next time, take care of yourself. Cheers.