What You Must Know About Business Cash Flow

70% of profitable companies still go bankrupt—are you making the same mistake? In this video, Steve explains why profit alone isn’t enough to keep your business alive—and reveals the one metric that truly determines financial health: free cash flow.

You’ll learn how to calculate it, why it matters more than you think, and how to avoid the cash flow traps that can cripple even successful businesses. If you want to protect your company and lead with confidence, this is a must-watch.

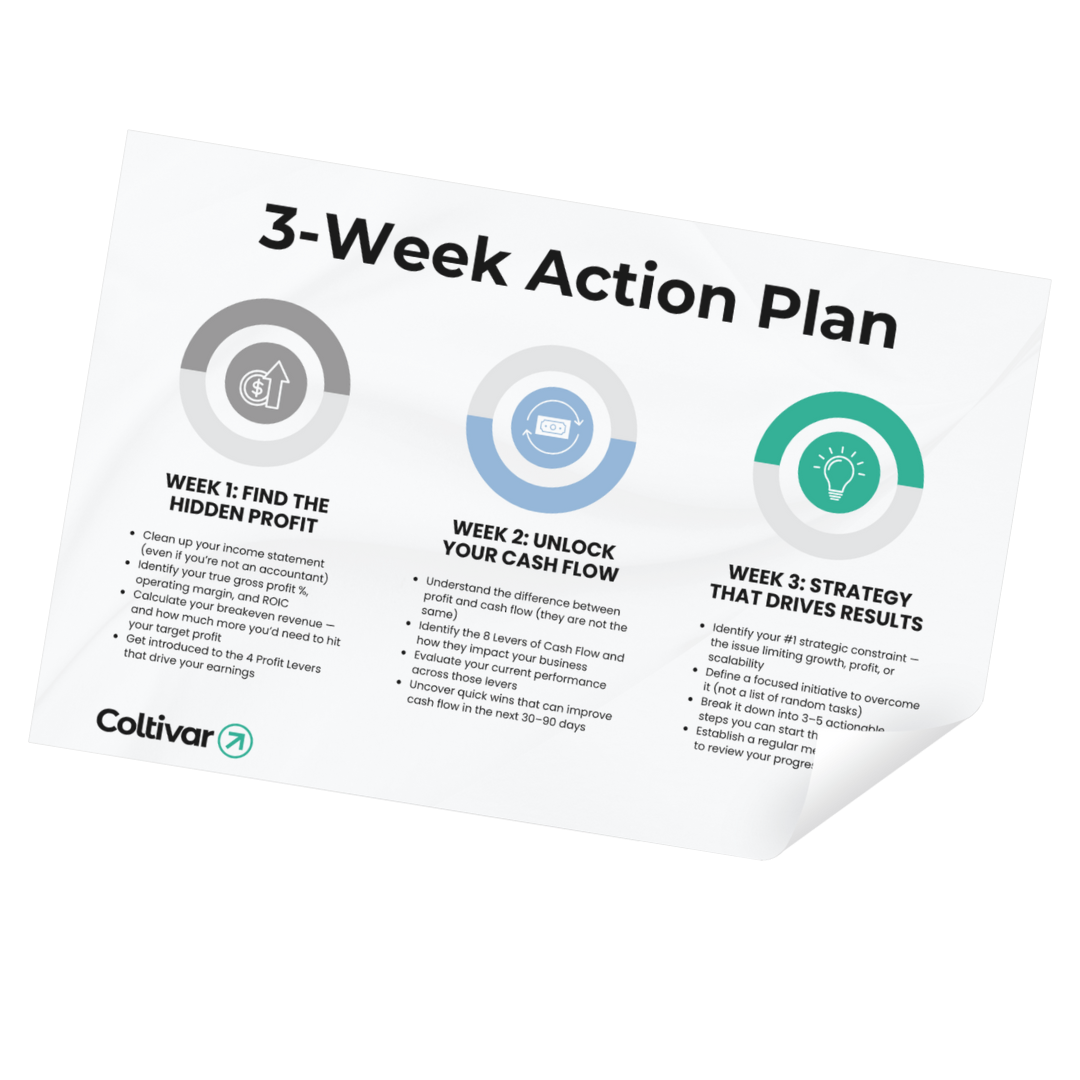

The 3-Week Plan to Grow Without Chaos

Learn how to take back control of your time, streamline your operations, and build a business that scales — without burning out.

Get my personalized planTRANSCRIPT:

A big fat 70% of companies that go bankrupt are actually profitable when they close their doors. In this video, I'm going to show you how that happens and what you need to compute in order to avoid the same trap in your organization. My name is Steve Coughran.

I'm the founder of Coltivar. I spent the last 15 years of my life turning around and growing companies, creating over a billion dollars in value in the process. Let's go ahead and jump in.

The problem exists because leaders mostly live on the income statement. It's not a bad financial statement, but it's incomplete for a lot of reasons. So let's break down the income statement and get down to free cashflow because that is the most important metric to be paying attention to.

Right. So if we begin with the income statement, it starts with revenue. This is also known as the top line of a company.

And it comes from the income that is produced from selling products and services. Underneath revenue, we have cost of goods sold. These are all the costs associated with fulfilling that revenue, material costs, direct labor, subcontractors, and all other direct and indirect costs related, like I said, to delivering those products or services into the hands of customers.

Underneath cost of goods sold, we have gross profit, also known as gross margin. This is the amount of profit a company earns by selling its products and services, fulfilling those products and services, and before accounting for overhead, which is next, which is just op-ex, which is short for operating expense, also known as selling general and administrative expense or SG&A or just G&A. But basically we're just talking about overhead.

The amount of cost a company incurs just to run the operations of the business, not to fulfill the product or service, that's up above in cost of goods sold, it's just running the company. General and administrative payroll, sales and marketing, insurance, professional fees, etc., all laying down here in operating expense. So if we take that revenue minus cost of goods sold, gross profit, gross profit minus op-ex, we end up with EBITDA.

And I'm just simplifying here. For some of you nerds who are like, Steve, that's not what it is. It's called operating profit.

I know, but I'm just keeping things really high level so we can understand how to get to cash flow. And really what I'm looking at is cash flow that is generated from the normal operations of the business. That's key, okay? So we have EBITDA, which is just a nerdy, fancy way of saying earnings before interest, taxes, depreciation, and amortization.

But in business, you get to subtract depreciation and amortization from the equation and then you arrive at earnings before interest and tax. The reason why we are not accounting for interest is because we want to ignore the capital structure of the company. In other words, maybe a company is financed with debt and therefore they pay interest on that debt, or maybe they're financed through equity.

So that's why we want to ignore interest at this point. And this will all make sense here at the end when I explain what free cash flow is all about, all right? So we have earnings before interest and tax. We just got rid of the depreciation and amortization.

Then the company will pay tax. And then after tax, we end up with net operating profit after tax. I'm just simplifying here.

I'm keeping things really high So this represents the amount of profit a company earns after taxes on the normal operations of the company. Because let's just say the business had a windfall because they sold a piece of equipment or they got discharged from paying back some PPP money, whatever it is. All those items are related to other income and other expense.

And we don't want to muddy up the waters here. We just want to focus on the amount of cash that a business is generating from operations. So that's why I'm excluding that stuff.

All right. So we have net operating profit after tax. This is where most business leaders live.

They either live up here in the EBITDA world or down here in net operating profit after tax or somewhere in between. But nonetheless, they look at their financial statements. They're like, huh, look, we're doing great.

Our EBITDA is up. We're making money. What's there to worry about? But remember, 70% of companies that go bankrupt are actually profitable when they close their doors.

So you could have profit, but not cash flow. And if that's your story, you go bust. So we have to keep going.

So we have net operating profit after tax, but depreciation and amortization is not a true cash flow item. It's not like a company writes a check to Mr. or Mrs. Depreciation or Amortization, right? This is just for tax purposes, because when a company buys a truck, look at my terrible truck, and let's just say it's 50 grand, you can't just record the 50 grand as an operating expense in one year. The IRS is like, no, you can't do that.

You have to match the economics of this truck to the financial statements. So instead, you have to say, this truck will last for five years, and it'll have a zero value after five years. I'm just making this up.

So therefore, 50,000 divided by five years is 10 Gs a year. And that's recorded as depreciation on this truck. And you do that every single year until the truck is worth zero on the books.

But that's not what we're getting into. I just want you to know what depreciation and amortization is. So we have to add it back, because we're trying to get to cash flow.

And like I said, it's not a cash flow item. So you go depreciation, amortization, we add it back. And if your head's hurting right now, don't worry, because at the end, I'm just going to show you the shortcut to computing free cash flow.

This is the long, nerdy way, but you should know the components anyways. So we have net operating profit after tax. We add back depreciation, amortization.

We account for changes in working capital. Working capital is really the difference between current assets and current liabilities. So you have inventory, prepaid, accounts receivable.

You have accounts payable over here. It's the difference between these two items. This is sitting on your balance sheet, but it's working capital.

It's where your money is tied up in the business. And then you have capital expenditures. So when you go out and buy trucks or pieces of equipment or a building for the business, that's known as CapEx, capital expenditures.

And you account for all these things. You take net operating profit after tax, add back depreciation and amortization, because it's not a true cash outflow. You account for working capital, and you also account for CapEx, and you arrive at free cash flow.

Yay. That was such a long way to get there. Maybe your head hurts.

Hopefully it doesn't. But cash flow, free cash flow, is the amount of cash that's available, number one, to pay down debt, number two, to return to equity providers through dividends or distributions, or three, to reinvest in the business, right? That's free cash flow. And that's what you could do with it in order to increase the value of a company.

Free cash flow is so important. In fact, that's how the intrinsic value of a company is determined. The intrinsic value of a company is basically the sum of all the future cash flow in today's dollars that a company or an asset will generate over its remaining useful life.

So as you can see, free cash flow not only keeps companies in business, but it also drives the value of a business. All right. As promised, I told you that I would give you the shortcut formula.

But before I do that, let me just give you a quick hack. If you're running a business here, one of the best things you could do is assign responsibility and accountability to every single line item on the financial statements down to free cash flow. In other words, you may come here and say, look, this is our sales manager's responsibility.

Tom, he's in charge of revenue. And Sarah, she's responsible for managing our costs for goods sold. And you go down the line and you assign each account one person.

And they are accountable to number one reporting on these numbers, but also for the strategies that will drive these numbers at the end of the day. So that has been a game changer. When I go into companies to turn them around or to grow them is assigned responsibility.

As promised, let me give you the shortcut here. If you just go to the statement of cash flows and you go to the first section, which is cash from operating activities. All right.

So if you take your operating cash and then you subtract out your capital expenditures, which can be found in the next section, right below cash from operating activities on the statement of cash flows. This is in your investing activities section. And you just take operating cash minus capex.

You arrive at free cash flow. And the reason why this works is because the statement of cash flows begins with net income. And then you add back non-cash items.

And then you also account for working capital. So it's just a shortcut to all this. This is the long version, the nerdy version.

And then this is the shortcut version. That's why the statement of cash flows is the most important financial statement. I love this financial statement and it will tell you everything you need to know in order to avoid getting crushed and going bankrupt in business.

If you need any help with your business, you can always go to cultivator.com to connect with us. Please be sure to share this if you found this valuable and until next time, take care of yourself. Cheers.